There is something especially cruel about the way this Administration talks about work.

It wraps itself in the language of entrepreneurship, grit, self-reliance, and “American job creators,” while targeting the very people who have spent years building businesses, hiring workers, and keeping local economies from hollowing out. This week, the U.S. Small Business Administration made that contradiction impossible to ignore.

According to a March 9 news release from the SBA, the agency has now expanded its restrictions on access to SBA-backed loans, banning foreign nationals and non-citizens from all SBA-guaranteed small business loan programs. That includes the agency’s Surety Bond and Microloan Programs, and it builds on an earlier policy change that had already made any small business owned in whole or in part by a foreign national ineligible for the SBA’s flagship 504 and 7(a) loan programs. Under the new rule, small business owners applying for any SBA loan program “must be U.S. citizens or U.S. nationals with their principal residence in the United States.”

“The Trump SBA is committed to driving economic growth and job creation for American citizens,” SBA Administrator Kelly Loeffler said in the agency’s release. “Last month, we made it clear that SBA would not allow foreign nationals to access our core small business loan programs, and today, we are expanding that policy to include all SBA-guaranteed loans. With our lending authority capped annually by Congress and amid record demand for access to capital, our responsibility is clear: the limited resource of SBA financing must prioritize American citizens who are building businesses and creating jobs here at home.”

On paper, the White House and the SBA want this to read as a simple America First correction. In practice, it reads as an attempt to choke off access to capital for immigrant communities, including a large swath of Latino entrepreneurs, at the precise moment they have become one of the country’s clearest engines of business growth.

What the SBA actually changed

According to Politico, the Small Business Administration issued policy guidance in early February requiring that all owners of a small business applying for the agency’s primary 7(a) loan program be U.S. citizens or U.S. nationals with principal residences in the United States. The outlet reported that the move rescinded a December policy that had allowed a 7(a) loan borrower to hold up to 5% of a business’s ownership by a foreign national, a green card holder, or a U.S. national or citizen living outside the country.

That shift was severe enough on its own. Green card holders who had permanent U.S. residency could no longer own any part of a business applying for the federal government’s most popular small business loan program. Then the Administration went further.

According to Reuters, the SBA notice stated that “Legal Permanent Residents (LPRs) will not be eligible to own any percentage interest in an Applicant/Borrower.”

Then came the March 9 expansion. According to the SBA’s own release, the rule now covers all SBA-guaranteed loans, including the Surety Bond Guarantee and Microloan programs. The agency said the change would take effect 30 days after publication.

The SBA said that in fiscal year 2025, it approved 3,358 loans for small businesses owned in part by lawful permanent residents, representing 4% of the agency’s total loan approvals of 85,000. Because Congress caps the agency’s lending authority each year, the SBA argued that “the limited resource of SBA financing must prioritize American citizens.”

But that framing leaves out the basic reality that lawful permanent residents are legal residents of the United States. They live here. They work here. They pay taxes here. They hire here. They build here. The Administration is asking the public to treat them as outsiders while depending on the economic life they help sustain.

Latino business owners already carry more of the economy than Washington admits

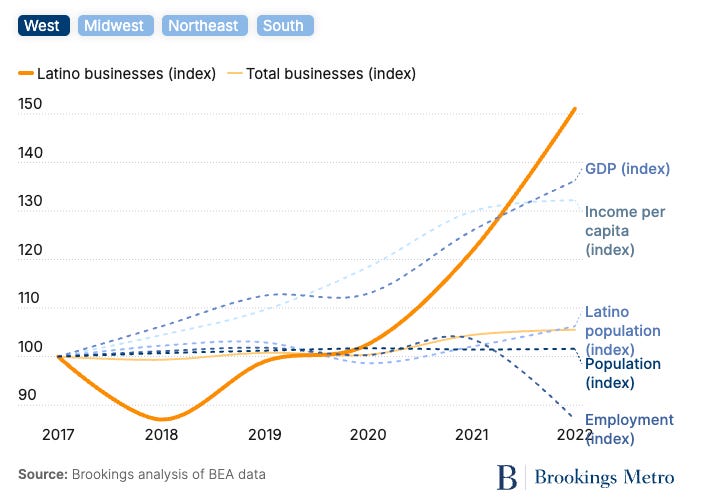

According to Brookings analysis of the Annual Business Survey, American Community Survey, and Bureau of Economic Analysis data from 2017 to 2022, Latino or Hispanic individuals owned 7.9% of all employer businesses in 2022, totaling 465,202 firms. Those businesses employed 3,550,230 people and generated more than $653 billion in total revenue. From 2021 to 2022 alone, Latino or Hispanic-owned businesses increased employment by 14.1% and total revenue by 18.9%.

That growth did not come out of nowhere. According to the same report, Latino or Hispanic-owned businesses grew at an average annual rate of 7.7% between 2017 and 2022, far outpacing the 0.46% growth rate for all employer businesses. Between 2017 and 2022, Latino or Hispanic-owned businesses grew in 204 of 227 U.S. metro areas studied. Between 2021 and 2022, they represented 58% of the increase in total employers nationwide.

This means that without Latino or Hispanic-owned businesses, the U.S. would have had 619,655 fewer jobs between 2019 and 2022, alongside a loss of $34 billion in workers’ wages and $190 billion in total revenue.

So when this Administration narrows access to capital in the name of protecting “American job creators,” it is attacking a sector of the business community that has already been doing the work of creating jobs, wages, and revenue at a pace the broader economy has struggled to match.

However, another point buried in the Brookings data deserves more attention. Latino or Hispanic business owners remain underrepresented relative to their share of the U.S. population. In 2022, Latino or Hispanic-identifying individuals made up 19.1% of the population but owned only 7.9% of employer businesses. According to Brookings, if the share of Latino or Hispanic-owned employer businesses matched the share of Americans who identify as Latino or Hispanic, there would be 812,440 more businesses generating a combined $1.1 trillion in revenue and $250 billion in payroll.

In other words, the country is already benefiting from Latino entrepreneurship while still starving it of the full room it deserves to grow.

And who gets shut out when Latino business owners lose access to capital?

The SBA does not need to name Latinos explicitly for Latino communities to feel the blow.

According to The Guardian, this is the first time in the agency’s history that legal residents, including green card holders, have been cut off from loans backed by the Small Business Administration. The paper reported that many of those loans support “main street” enterprises such as retail shops, restaurants, cafes, franchises, and business-to-business services in sectors ranging from manufacturing to transportation.

That description should sound familiar to anyone who knows how Latino entrepreneurship actually looks on the ground. It is the restaurant owner trying to expand, the contractor trying to bid on a larger project. The family business struggling to buy equipment. The franchisee who wants to open a first location.

According to The Guardian, Keegan McBride, co-founder of SBA Source, said many franchisees are immigrants, including both green card holders and naturalized U.S. citizens, and that under the new rule, even married couples trying to launch a business together could be blocked from an SBA loan if both people are not U.S. citizens. He explained why these loans matter by saying, “SBA loans are really only meant to be issued in situations where folks wouldn’t be able to get access to credit on similar terms without the government guarantee. It’s challenging because SBA is kind of designed to fill that gap.”

That gap is the story. Conventional lenders already reward people who have home equity, inherited wealth, investment portfolios, or the kind of financial cushion that makes risk feel manageable. SBA-backed loans were created to reach people who do not move through the economy with those protections.

Many Latino families know that terrain intimately. They build businesses while carrying less generational wealth, thinner margins, and fewer institutional connections. Cutting off access to government-backed financing does not level the playing field. It tilts it even harder toward the people who already own most of it.

The Administration says this protects Americans. The record says something else.

The Administration has not been subtle about the worldview behind this policy.

According to Politico, the change is consistent with Trump’s January 2025 executive order on “protecting the American people against invasion,” which directs federal agencies to “employ all lawful means to ensure the faithful execution of the immigration laws of the United States.” According to Lexology’s review of the policy changes, the SBA’s tightening rules have been gradual, beginning in 2025 and becoming more restrictive over time, culminating in a February 2026 policy that excludes legal permanent residents from owning even 1% of a business applying for SBA-backed financing.

This was not a one-off administrative correction. It was a deliberate campaign to tether access to capital to the Administration’s broader immigration enforcement agenda.

In an op-ed posted to the SBA’s website in February, Loeffler said, “Trump has restored confidence and opportunity to Main Street with a commonsense economic agenda designed to put hardworking families and small businesses, not Washington bureaucrats, illegal aliens or coastal elites, in the driver’s seat,” according to The Guardian.

But the policy does not stop at undocumented immigrants. It reaches legal permanent residents. It reaches people whom the government itself has authorized to live and work permanently in the United States. It reaches people who have built businesses, paid taxes, created jobs, and committed themselves to this country for years.

According to Politico, Sen. Ed Markey and Rep. Nydia Velázquez said in a joint statement: “The Trump administration is stoking the flames of hatred, spreading fear and confusion among immigrants and small business owners. Rather than support hardworking legal immigrants to start or expand a business, the Trump SBA is choosing hatred by barring green card holders from receiving an SBA loan. The Administration’s message to immigrants is clear: you are not welcome to pursue the American Dream.”

According to The Guardian, Aissatou Barry-Fall, CEO of the Lower East Side People’s Federal Credit Union, said the new policy makes “no sense whatsoever” and added, “I think it’s discrimination. That’s all it is.”

Latino business owners grew across the country. The punishment is national too.

One of the laziest myths in American politics is that Latino economic power is confined to a few predictable places. The data says otherwise.

According to Brookings, Latino or Hispanic-owned businesses grew in nearly 90% of the metro areas examined between 2017 and 2022. The biggest numerical gains came in places with large Latino communities, including Miami, Los Angeles, and New York. Miami alone added 13,693 Latino or Hispanic-owned businesses during that period. Los Angeles added 10,999. New York added 8,727.

And yet the pattern was national. Growth was observed across the Midwest and parts of the Southern Appalachians. Latino or Hispanic-owned businesses also contributed heavily to overall business growth in major metro areas. According to Brookings, they accounted for over 93% of total growth in Miami, 47% in Los Angeles, and 65% in Orlando.

These businesses are concentrated in sectors that shape everyday life. In 2022, according to Brookings, Latino or Hispanic-owned employer businesses were clustered in construction, accommodation and food services, and professional, scientific, and technical services. From 2017 to 2022, Latino- or Hispanic-owned construction businesses increased by over 37,500, a 75% jump. Transportation and warehousing grew by 74%. Arts, entertainment, and recreation grew by 86%. Real estate and rental leasing grew by 66%.

So why target Latino business owners now?

Because capital is power.

A community that starts businesses builds more than income. It builds autonomy. It builds leverage. It builds local hiring power, local political influence, neighborhood stability, and the ability to survive institutions that were never designed to make life easy. Small business formation changes the social map of who gets to own, employ, and endure.

That helps explain why this Administration keeps returning to the same pressure points: Immigration status. Access to credit. Federal legitimacy. The right to belong economically.

According to the SBA’s March 9 release, the agency also pointed to earlier efforts, including citizenship verification requirements across its loan programs, to “cut off access to loans for illegal aliens” and plans to move SBA field offices out of sanctuary cities that it says do not comply with ICE. In other words, this is a political worldview being translated into administrative barriers.

And it arrives at a brutal time. According to Politico, small business advocates warned that restrictions on green card holders come as small businesses are already struggling with tariffs, health care costs, inflation, and long-standing difficulties accessing capital. Small Business Majority founder and CEO John Arensmeyer said the decision “will limit the growth of small businesses and jobs throughout the United States” and that “the timing of SBA’s tighter lending eligibility criteria could not be worse.” He called on the agency to “prioritize broadening eligibility rather than narrowing it.”

According to The Guardian, restaurateur Aneesa Waheed, who was named the SBA’s New York state small business person of the year in 2024, put the emotional reality of the shift into plain language. “I’m really shocked,” she said. “I’ve been in the SBA world for a long time. You think of the SBA as a source of support and strength for small businesses.”

For decades, the SBA was one of the few places where the federal government acknowledged that access to capital should not be limited exclusively to the already secure. Now the agency is being used to narrow who counts as fully investable in America.

What they are really cutting off

There is a temptation to describe this as an immigration story and leave it there. That would let the Administration off too easily.

This is also a labor story. A wealth story. A race story. A story about who gets to convert work into ownership.

According to Reuters, the new rule does not stop non-citizens from owning businesses in the United States or from accessing conventional bank loans. That is true. It is also incomplete. Conventional credit is often harder to obtain, especially for founders without the collateral, asset base, or financial history that banks prefer. That is exactly why SBA-backed loans exist.

According to The Guardian, McBride said that without the SBA guarantee, many borrowers will have to rely on home equity, investment portfolios, or other forms of collateral to secure financing. Those are resources that many working and immigrant families do not have in abundance.

This is where the broader economic picture comes back into view. Brookings found that Latino or Hispanic-owned businesses likely buffered the U.S. economy against a more severe downturn during and after the pandemic. They helped drive post-pandemic business creation. They generated jobs, wages, and revenue in places that badly needed all three.

And still, they remain underrepresented. Still, there is room for growth. Still, the ceiling has not remotely been reached.

So when this Administration closes off a critical financing pathway, it’s telling a fast-growing entrepreneurial community that its labor, taxes, hiring, and revenue are welcome, but its claim to institutional support remains conditional.

{kind=link}